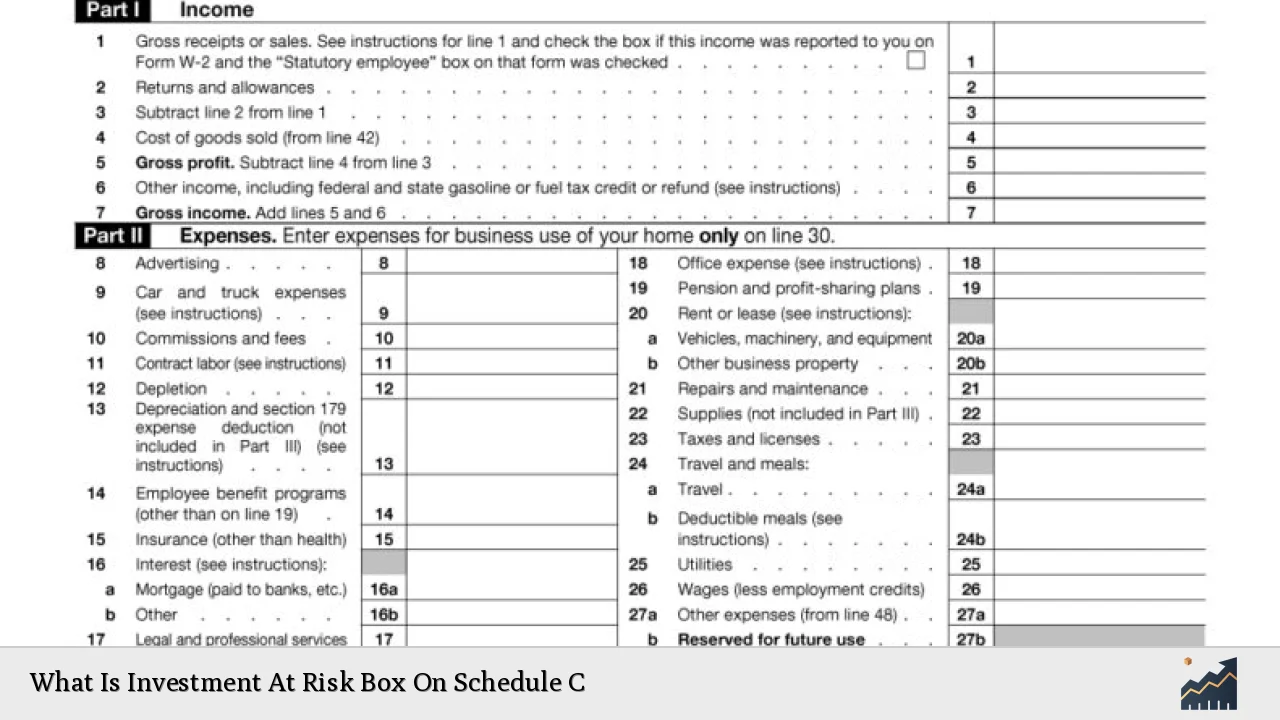

The “Investment at Risk” box on Schedule C is a critical component for sole proprietors and small business owners when reporting their business income and expenses to the IRS. This section is designed to assess the amount of investment that an individual is personally at risk of losing in the event of a business failure. Understanding this concept is essential for accurately reporting losses and ensuring compliance with tax regulations.

The IRS imposes at-risk rules to limit the amount of loss a taxpayer can claim to what they could realistically lose in their business. If an individual has invested money in their business, they can only deduct losses up to the amount they have personally invested or are liable for, which is referred to as their at-risk basis. This prevents taxpayers from claiming excessive losses that exceed their actual financial exposure.

| Key Concept | Description/Impact |

|---|---|

| At-Risk Rules | Limits loss deductions to the amount personally invested or liable for; prevents claiming losses beyond actual financial exposure. |

| Personal Liability | Investments made with borrowed funds are considered at risk only if the taxpayer is personally liable for repayment. |

| Suspended Losses | If losses exceed the at-risk investment, the excess is suspended and can be carried forward to future tax years. |

| IRS Form 6198 | This form must be completed if any part of the investment is not at risk, detailing the limitations on loss deductions. |

| Schedule C Reporting | Schedule C is used by sole proprietors to report income and expenses; accurate reporting of at-risk investments is crucial for tax compliance. |

Market Analysis and Trends

The landscape of small business investments has evolved significantly, particularly in light of recent economic conditions. The following trends are noteworthy:

- Increased Borrowing: Many small businesses have turned to loans to finance operations, which raises questions about personal liability and at-risk calculations. As interest rates remain elevated, understanding how these loans impact personal risk is crucial.

- Economic Recovery: Post-pandemic recovery has seen many entrepreneurs re-entering the market. However, they must navigate complex tax implications related to their investments.

- Regulatory Changes: Ongoing changes in tax regulations require business owners to stay informed about how these adjustments affect their at-risk calculations.

Implementation Strategies

To effectively manage investments and comply with at-risk rules, business owners should consider the following strategies:

- Maintain Accurate Records: Keep detailed records of all investments made in the business, including personal contributions and loans. This documentation will support claims made on Schedule C.

- Understand Personal Liability: Evaluate whether any borrowed funds used for business operations are personally guaranteed. This status affects what portion of those funds can be considered “at risk.”

- Consult Tax Professionals: Given the complexities surrounding at-risk rules, consulting with a tax advisor can help ensure compliance and optimize tax strategies.

Risk Considerations

Investing in a small business inherently carries risks that must be understood and managed:

- Market Volatility: Economic fluctuations can impact revenue streams, affecting the potential for losses that may exceed at-risk investments.

- Debt Management: High levels of borrowing can increase personal liability, influencing how much capital is considered at risk.

- Regulatory Compliance: Failure to comply with IRS regulations regarding at-risk investments can lead to penalties or disallowed deductions.

Regulatory Aspects

The IRS has established specific guidelines regarding at-risk investments:

- IRS Publication 535: This publication outlines deductible business expenses and details how at-risk rules apply to various forms of investment.

- Form 6198: Business owners must complete this form if they have amounts invested that are not considered at risk. It calculates allowable loss deductions based on personal exposure.

- State Regulations: In addition to federal guidelines, state tax laws may impose additional requirements concerning investment reporting and deductions.

Future Outlook

Looking ahead, several factors will influence how investors approach the “Investment At Risk” box on Schedule C:

- Interest Rate Trends: As central banks navigate inflationary pressures, interest rates will likely remain a key factor affecting borrowing costs and investment strategies.

- Economic Conditions: The overall economic environment will dictate consumer behavior and business performance, impacting potential losses that may need to be reported.

- Tax Reform Discussions: Ongoing discussions about tax reform could lead to changes in how at-risk investments are treated, necessitating vigilance from investors.

Frequently Asked Questions About Investment At Risk Box On Schedule C

- What does “at risk” mean on Schedule C?

The term “at risk” refers to the amount of money you could lose in your business. You can only deduct losses up to this amount. - How do I determine my at-risk basis?

Your at-risk basis includes your cash investment plus any loans for which you are personally liable. - What happens if my losses exceed my at-risk investment?

If your losses exceed your at-risk investment, the excess loss becomes a suspended loss that can be carried forward to future years. - Do I need to file Form 6198?

You must file Form 6198 if any part of your investment is not considered at risk. - Can I deduct all my business losses?

No, you can only deduct losses up to the amount you have personally invested or are liable for. - How often do I need to reassess my at-risk basis?

You should reassess your at-risk basis annually or whenever you make significant changes to your investment structure. - What types of investments are not considered at risk?

Investments where you have no personal liability or where third-party guarantees exist are typically not considered at risk. - Is it advisable to consult a tax professional regarding my investments?

Yes, consulting a tax professional can provide clarity on complex regulations and help optimize your tax situation.

Understanding the “Investment At Risk” box on Schedule C is essential for accurately reporting your business’s financial health while maximizing potential tax benefits. By staying informed about market trends, implementing effective strategies, considering risks, adhering to regulatory requirements, and anticipating future changes, investors can navigate this complex landscape with confidence.