Investing wisely not only helps you grow your wealth but can also significantly reduce your taxable income. Understanding which investments offer tax benefits is crucial for maximizing your financial returns while minimizing your tax liabilities. Various strategies and investment vehicles can help you achieve this goal, from tax-advantaged accounts to specific types of securities. This article explores the most effective investments that can help reduce your taxable income.

| Investment Type | Tax Benefit |

|---|---|

| Retirement Accounts (e.g., IRA, 401(k)) | Contributions may be tax-deductible, and earnings grow tax-deferred. |

| Municipal Bonds | Interest income is often exempt from federal and sometimes state taxes. |

Tax-Advantaged Retirement Accounts

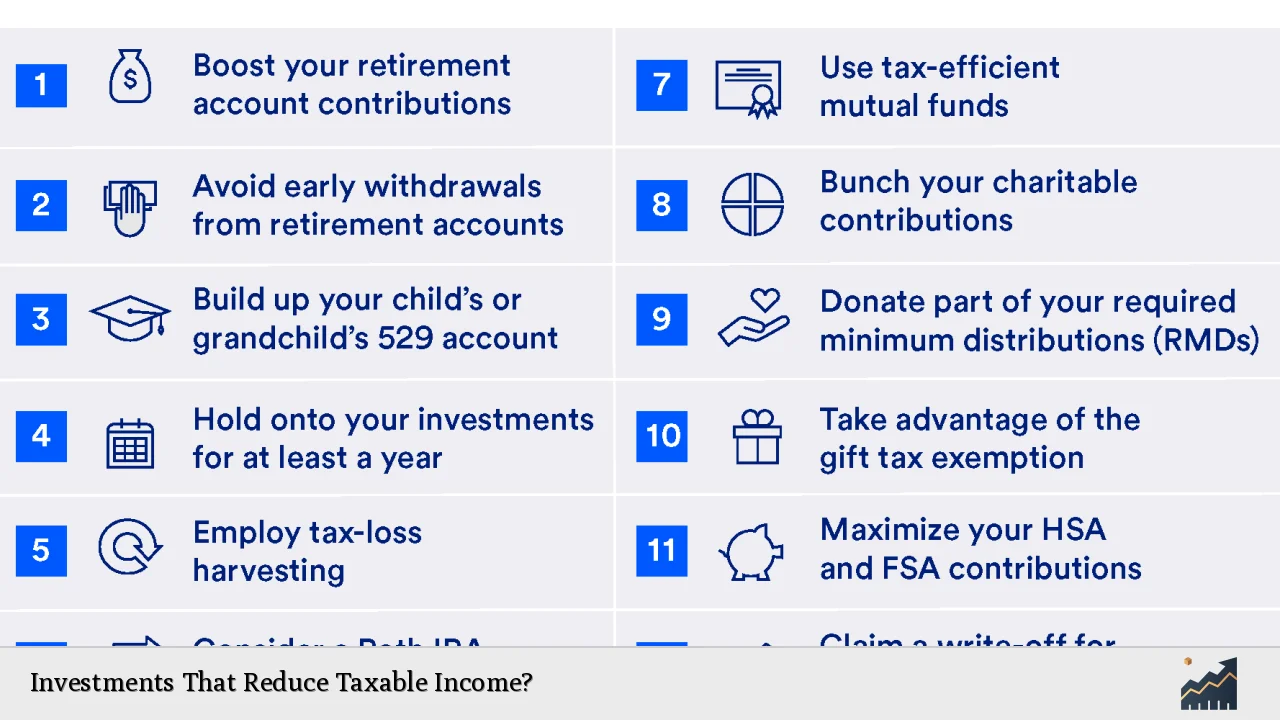

One of the most effective ways to reduce taxable income is through tax-advantaged retirement accounts. These accounts allow you to invest money that can grow without being taxed until you withdraw it, typically during retirement when you may be in a lower tax bracket.

- Traditional IRA: Contributions to a Traditional IRA may be tax-deductible depending on your income and whether you have access to an employer-sponsored retirement plan. The money grows tax-deferred until you withdraw it in retirement.

- 401(k) Plans: Similar to IRAs, contributions to a 401(k) are made pre-tax, reducing your taxable income for the year. Many employers also match contributions, effectively increasing your investment.

- Roth IRA: While contributions are made with after-tax dollars, qualified withdrawals are tax-free, providing a significant benefit if you expect to be in a higher tax bracket in retirement.

These accounts not only help in reducing current taxable income but also provide long-term growth opportunities without immediate tax implications.

Municipal Bonds

Investing in municipal bonds is another effective strategy for reducing taxable income. These bonds are issued by state and local governments and are generally exempt from federal taxes. In some cases, they may also be exempt from state taxes if you reside in the state where the bond was issued.

- Tax-Exempt Interest: The interest earned on municipal bonds is often exempt from federal income tax, making them attractive for investors in higher tax brackets who want to preserve their after-tax returns.

- Lower Yield: While municipal bonds typically offer lower yields than taxable bonds, the tax benefits can make them more appealing for certain investors.

This strategy is particularly beneficial for those seeking stable income without the burden of high taxes on interest earnings.

Tax-Efficient Funds

Investors should consider tax-efficient funds, such as index funds and exchange-traded funds (ETFs). These funds are designed to minimize capital gains distributions and other taxable events that can increase your tax bill.

- Index Funds: By tracking a specific market index, these funds do not engage in frequent trading, which reduces capital gains distributions. This makes them inherently more tax-efficient compared to actively managed funds.

- ETFs: Similar to index funds, ETFs typically have lower turnover rates. Additionally, when you sell an ETF share, you’re selling it to another investor rather than the fund itself, which helps avoid triggering capital gains within the fund.

Choosing these types of investments can lead to significant savings on taxes over time while still providing exposure to market growth.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy that involves selling investments at a loss to offset gains realized on other investments. This practice can effectively reduce your overall taxable income by lowering your capital gains liability.

- Offset Gains: If you’ve realized gains from selling an investment, you can sell another investment at a loss to offset those gains. For instance, if you have a $10,000 gain and an $8,000 loss, you’ll only pay taxes on the net gain of $2,000.

- Carry Forward Losses: If your losses exceed your gains in a given year, you can carry forward the unused losses to future years. This allows for continued tax savings as you realize gains in subsequent years.

This strategy requires careful planning but can yield substantial tax benefits when executed correctly.

Real Estate Investments

Investing in real estate can also provide significant tax advantages. The IRS allows property owners to deduct various expenses related to property ownership and management.

- Depreciation Deductions: Real estate investors can deduct depreciation on their properties over time. This non-cash deduction reduces taxable income significantly while allowing the investor to maintain cash flow from rental income.

- 1031 Exchange: Under Section 1031 of the IRS code, investors can defer capital gains taxes by reinvesting proceeds from the sale of one investment property into another similar property. This strategy allows investors to grow their portfolios without immediate tax implications.

Real estate investments not only provide potential appreciation but also offer various deductions that help reduce taxable income.

Health Savings Accounts (HSAs)

A Health Savings Account (HSA) is another excellent tool for reducing taxable income while preparing for future medical expenses. HSAs offer unique triple-tax advantages:

- Tax-Deductible Contributions: Contributions made to an HSA are deductible from your taxable income, reducing your overall tax burden for the year.

- Tax-Free Growth: Funds in an HSA grow tax-free as long as they remain in the account.

- Tax-Free Withdrawals for Qualified Expenses: Withdrawals made for qualified medical expenses are not taxed at all.

This makes HSAs particularly beneficial for individuals with high-deductible health plans looking to save for future healthcare costs while enjoying immediate tax benefits.

Charitable Contributions

Making charitable contributions is not only a way to give back but also an effective method for reducing taxable income. Donations made to qualified charitable organizations can be deducted from your taxable income if you itemize deductions on your tax return.

- Cash Donations: Cash donations made directly to charities are deductible up to 60% of your adjusted gross income (AGI).

- Non-Cash Donations: Donating appreciated assets like stocks or real estate allows you to avoid paying capital gains taxes on those assets while still claiming a deduction based on their fair market value at the time of donation.

This dual benefit makes charitable giving an appealing option for those looking to support causes they care about while reducing their overall tax liability.

FAQs About Investments That Reduce Taxable Income

- What is a tax-efficient investment?

A tax-efficient investment minimizes taxes owed on returns through strategies like low turnover and holding periods. - How do retirement accounts reduce taxable income?

Contributions to retirement accounts such as IRAs and 401(k)s may be deductible from current taxable income. - Can I deduct losses from my investments?

Yes, losses can offset gains through tax-loss harvesting strategies. - What are municipal bonds?

Municipal bonds are debt securities issued by governments that often provide interest exempt from federal taxes. - How do HSAs work for taxes?

HSAs offer deductible contributions, tax-free growth, and withdrawals for qualified medical expenses without taxation.

In summary, various investment strategies exist that can significantly reduce your taxable income. Utilizing retirement accounts, municipal bonds, tax-efficient funds, real estate investments, HSAs, and charitable contributions provides multiple avenues for minimizing taxes while building wealth. By understanding these options and implementing them effectively within your financial plan, you can optimize both your investment returns and your overall financial health.