The introduction of the New Tax Regime in India has significantly altered the landscape for individual taxpayers. This regime, first proposed in the Union Budget of 2020-21, offers lower tax rates but requires taxpayers to forgo many deductions and exemptions that were available under the old system. As a result, individuals must carefully consider their investment strategies to optimize their tax liabilities while achieving their financial goals.

The New Tax Regime has been designed to simplify tax compliance and encourage more taxpayers to opt for it by providing a more straightforward structure with fewer tax slabs. However, understanding how to navigate this new framework is crucial for maximizing benefits. This article explores various investment options that can be effectively utilized within the New Tax Regime, detailing how they can help reduce tax liabilities and enhance financial outcomes.

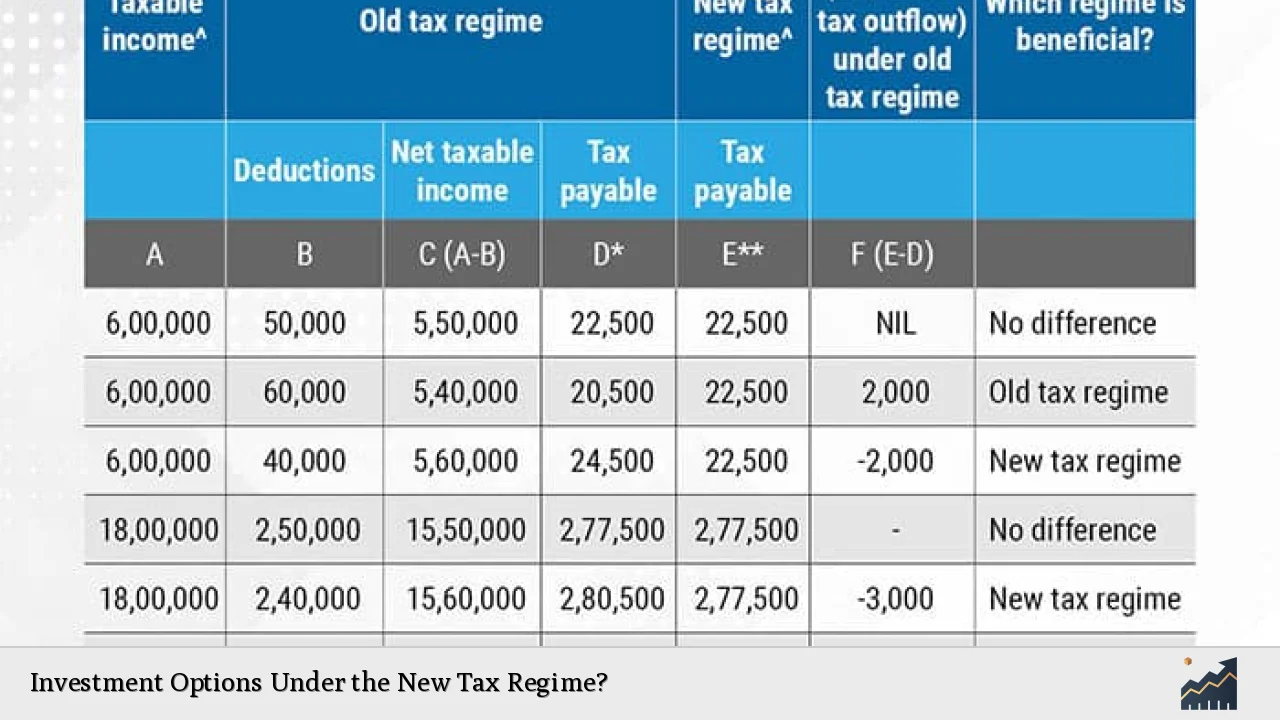

| Investment Type | Tax Benefit |

|---|---|

| National Pension System (NPS) | Deductions under Section 80CCD |

| Public Provident Fund (PPF) | Deductions under Section 80C |

| Equity Linked Savings Scheme (ELSS) | Deductions under Section 80C |

| Fixed Deposits (FDs) | Deductions under Section 80C |

Understanding the New Tax Regime

The New Tax Regime has been implemented with the intent to simplify the taxation process for individuals. It features a reduced number of tax slabs and lower rates compared to the old regime. The main highlights include:

- Basic Exemption Limit: The basic exemption limit has been raised to ₹3 lakh, allowing individuals with income up to this threshold to pay no tax.

- Tax Rebate: A full tax rebate is available for individuals earning up to ₹7 lakh, effectively making their income tax liability zero.

- Standard Deduction: The introduction of a standard deduction of ₹50,000 has been a significant benefit for salaried taxpayers.

- Fewer Deductions: Unlike the old regime, which allows numerous deductions under various sections like 80C, 80D, etc., the new regime limits these options, making it essential for taxpayers to choose investments wisely.

The government aims to encourage taxpayers to transition to this regime by simplifying compliance and reducing overall tax burdens. However, individuals must evaluate whether opting for this regime aligns with their financial strategies.

Investment Strategies Within the New Tax Regime

To make the most of the New Tax Regime, taxpayers can consider several investment options that not only provide tax benefits but also contribute towards long-term financial goals. Here are some effective strategies:

National Pension System (NPS)

The National Pension System is an excellent investment avenue for retirement planning. Under this scheme:

- Contributions made towards NPS are eligible for deductions under Section 80CCD.

- An additional deduction of up to ₹50,000 is available specifically for NPS contributions beyond the limit set by Section 80C.

- NPS investments offer flexibility in choosing between equity and debt funds, allowing investors to align their portfolios with their risk appetite.

This makes NPS a compelling option for individuals looking to save on taxes while securing their financial future.

Public Provident Fund (PPF)

The Public Provident Fund remains a popular choice due to its safety and attractive interest rates. Key features include:

- Contributions are eligible for deductions under Section 80C, up to a maximum of ₹1.5 lakh per annum.

- The interest earned and maturity amount are completely tax-free.

- PPF accounts have a lock-in period of 15 years, making them suitable for long-term savings.

Investing in PPF can provide stability and guaranteed returns while offering significant tax benefits.

Equity Linked Savings Scheme (ELSS)

ELSS funds are mutual funds that invest primarily in equities and come with a lock-in period of three years. They offer:

- Deductions under Section 80C, allowing investments up to ₹1.5 lakh per annum.

- Historically higher returns compared to traditional fixed-income instruments, making them suitable for investors willing to take on some risk.

- The potential for capital appreciation over time, which can significantly enhance wealth creation.

For those looking at aggressive growth while saving on taxes, ELSS is an attractive option.

Fixed Deposits (FDs)

Tax-saving fixed deposits are another avenue worth considering:

- These FDs offer deductions under Section 80C, similar to PPF and ELSS, but come with a lock-in period of five years.

- While they provide lower returns compared to equity investments, they offer guaranteed returns and are suitable for conservative investors.

Investing in FDs can be part of a diversified portfolio that balances risk and return while ensuring tax benefits.

Evaluating Your Options

When deciding which investment options to pursue under the New Tax Regime, consider your financial goals, risk tolerance, and investment horizon.

- If you prioritize liquidity and flexibility, options like ELSS or NPS may suit you better.

- For guaranteed returns with minimal risk, PPF or tax-saving FDs might be more appropriate.

It’s also essential to regularly review your investments and adjust your strategy based on changes in your financial situation or shifts in government policy regarding tax regulations.

FAQs About Investment Options Under the New Tax Regime

- What is the basic exemption limit under the new tax regime?

The basic exemption limit is ₹3 lakh. - How much can I save through NPS contributions?

You can claim deductions up to ₹1.5 lakh under Section 80CCD. - Are ELSS funds safe investments?

While ELSS funds have potential for higher returns, they are subject to market risks. - What is the lock-in period for PPF?

The lock-in period for PPF is 15 years. - Can I switch back to the old tax regime after opting for the new one?

You can switch back only at the time of filing your income tax return.

In conclusion, navigating the New Tax Regime requires careful consideration of available investment options. By strategically selecting investments such as NPS, PPF, ELSS, and fixed deposits, taxpayers can optimize their tax liabilities while working towards their broader financial objectives.