Retirement planning is a crucial financial goal that requires careful consideration and strategic investment. The amount you need to invest for retirement depends on various factors, including your current age, desired retirement age, expected lifestyle, and anticipated expenses. While there’s no one-size-fits-all answer, understanding key principles and guidelines can help you determine how much to invest quickly for a comfortable retirement.

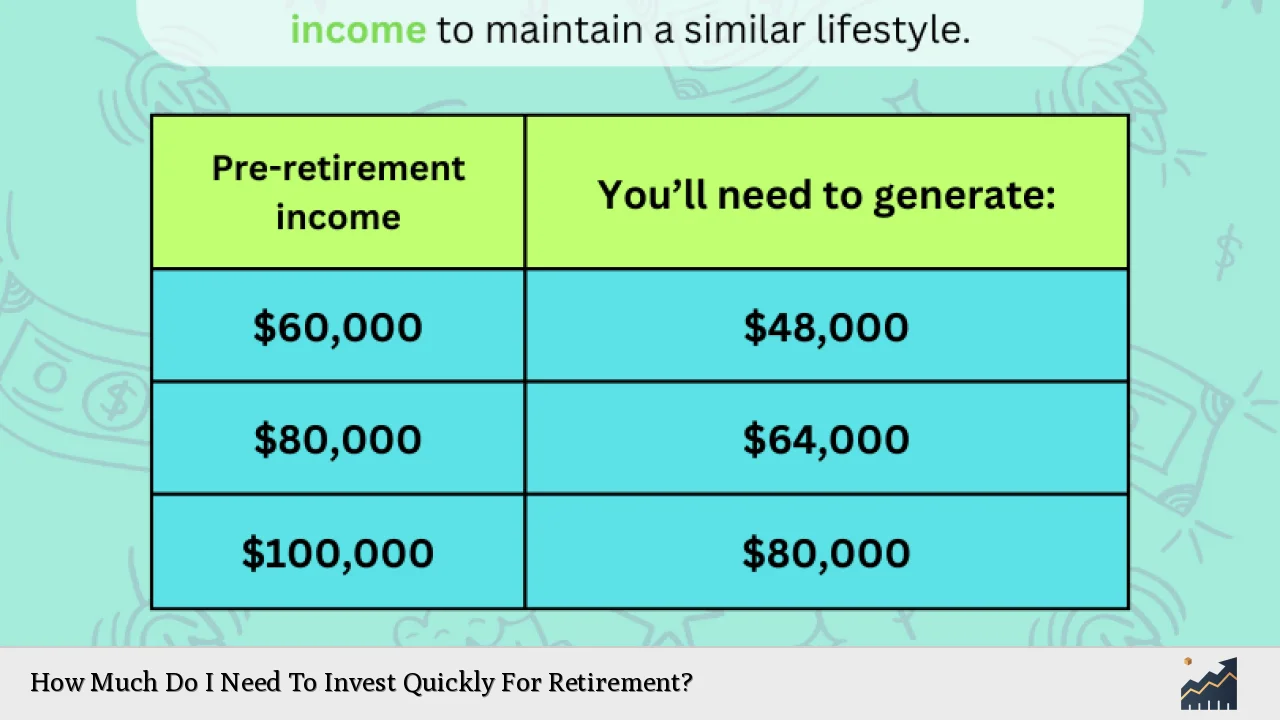

To get a quick estimate of how much you might need to save for retirement, financial experts often recommend using the “25x rule” or the “4% rule.” This guideline suggests that you should aim to save 25 times your desired annual retirement income. For example, if you want to have $80,000 per year in retirement, you would need to save approximately $2 million ($80,000 x 25).

| Desired Annual Retirement Income | Estimated Retirement Savings Goal |

|---|---|

| $40,000 | $1,000,000 |

| $60,000 | $1,500,000 |

| $80,000 | $2,000,000 |

| $100,000 | $2,500,000 |

Factors Affecting Retirement Investment Needs

Several key factors influence how much you need to invest for retirement:

1. Current Age and Retirement Age: The earlier you start investing, the more time your money has to grow through compound interest. If you’re starting later in life, you may need to invest more aggressively to catch up.

2. Life Expectancy: With increasing life expectancies, it’s essential to plan for a longer retirement period. Many financial advisors recommend planning for at least 30 years of retirement.

3. Lifestyle Expectations: Your desired lifestyle in retirement significantly impacts how much you need to save. Consider factors like travel, hobbies, and healthcare costs.

4. Inflation: Remember that the cost of goods and services typically increases over time. Your retirement savings should account for inflation to maintain your purchasing power.

5. Social Security Benefits: While Social Security can provide some income in retirement, it’s generally not enough to cover all expenses. Consider it as a supplement to your retirement savings.

6. Healthcare Costs: As you age, healthcare expenses often increase. It’s crucial to factor in potential medical costs, including long-term care.

7. Investment Returns: The rate of return on your investments can significantly impact how quickly your retirement savings grow. A higher return may allow you to invest less, while a lower return might require larger contributions.

Quick Investment Strategies for Retirement

If you’re looking to invest quickly for retirement, consider these strategies:

1. Maximize Employer-Sponsored Plans: If your employer offers a 401(k) or similar retirement plan, contribute the maximum amount possible, especially if there’s an employer match. This is essentially free money that can significantly boost your retirement savings.

2. Open an IRA: In addition to employer-sponsored plans, consider opening an Individual Retirement Account (IRA). For 2024, you can contribute up to $7,000 to an IRA ($8,000 if you’re 50 or older).

3. Utilize Catch-Up Contributions: If you’re 50 or older, take advantage of catch-up contributions. In 2024, you can contribute an additional $7,500 to your 401(k) and $1,000 to your IRA.

4. Invest in Low-Cost Index Funds: These funds offer broad market exposure and typically have lower fees than actively managed funds, allowing more of your money to grow over time.

5. Consider a Roth IRA: While contributions are made with after-tax dollars, withdrawals in retirement are tax-free. This can be particularly beneficial if you expect to be in a higher tax bracket in retirement.

6. Automate Your Investments: Set up automatic transfers from your paycheck or bank account to your retirement accounts. This ensures consistent investing and takes advantage of dollar-cost averaging.

7. Reduce High-Interest Debt: Before aggressively investing, pay off high-interest debt like credit card balances. The interest saved can be redirected towards retirement savings.

Calculating Your Retirement Investment Needs

To determine how much you need to invest quickly for retirement, follow these steps:

1. Estimate Your Retirement Expenses: Calculate your expected annual expenses in retirement, including essentials like housing, food, and healthcare, as well as discretionary spending.

2. Account for Inflation: Adjust your estimated expenses for inflation. A common rule of thumb is to use a 3% annual inflation rate.

3. Determine Your Retirement Income Sources: Consider Social Security benefits, pensions, and any other expected income sources in retirement.

4. Calculate the Shortfall: Subtract your expected retirement income from your estimated expenses to determine how much you need to cover through investments.

5. Use the 25x Rule: Multiply your annual shortfall by 25 to get a rough estimate of how much you need to save.

6. Factor in Time Until Retirement: The less time you have until retirement, the more aggressively you’ll need to save and invest.

7. Consult a Financial Advisor: For a more personalized and accurate assessment, consider working with a financial advisor who can take into account your specific situation and goals.

Balancing Risk and Return in Retirement Investments

When investing quickly for retirement, it’s crucial to balance risk and potential returns:

1. Diversification: Spread your investments across different asset classes (stocks, bonds, real estate) to manage risk.

2. Asset Allocation: Adjust your portfolio based on your risk tolerance and time horizon. Generally, younger investors can afford to take on more risk with a higher allocation to stocks.

3. Regular Rebalancing: Periodically review and adjust your portfolio to maintain your desired asset allocation.

4. Consider Target-Date Funds: These funds automatically adjust their asset allocation as you approach retirement, becoming more conservative over time.

5. Stay Informed: Keep up with market trends and economic conditions, but avoid making rash decisions based on short-term market fluctuations.

Remember, while investing quickly for retirement is important, it’s equally crucial to invest wisely. Avoid taking on unnecessary risks in an attempt to catch up, as this could potentially jeopardize your retirement savings.

FAQs About How Much To Invest Quickly For Retirement

- How much should I save each month for retirement?

Aim to save at least 15% of your gross income, including any employer contributions. - Is it too late to start saving for retirement at 50?

It’s never too late, but you’ll need to save more aggressively and take advantage of catch-up contributions. - Should I prioritize paying off debt or saving for retirement?

Focus on high-interest debt first, then balance between debt repayment and retirement savings. - Can I rely solely on Social Security for retirement?

Social Security alone is typically not enough; it’s designed to supplement other retirement savings. - How often should I review my retirement investment strategy?

Review annually or when experiencing significant life changes to ensure your strategy remains aligned with your goals.