The Thrift Savings Plan (TSP) is a powerful retirement savings tool for federal employees and members of the uniformed services. Investing your TSP effectively can significantly impact your financial future. To make the most of your TSP, it’s crucial to understand your investment options and develop a strategy that aligns with your retirement goals and risk tolerance.

The TSP offers several investment funds, each with its own risk and return profile. These funds include the G Fund (Government Securities), F Fund (Fixed Income Index), C Fund (Common Stock Index), S Fund (Small Cap Stock Index), and I Fund (International Stock Index). Additionally, the TSP provides Lifecycle (L) Funds, which automatically adjust your investment mix based on your target retirement date.

To help you get started, here’s a quick overview of the TSP funds and their characteristics:

| Fund | Description |

|---|---|

| G Fund | Low risk, government securities |

| F Fund | U.S. bond market index fund |

| C Fund | Large-cap U.S. stock index fund |

| S Fund | Small-cap U.S. stock index fund |

| I Fund | International stock index fund |

Now, let’s dive into the key strategies for investing your TSP effectively.

Diversify Your TSP Portfolio

One of the most important principles of investing is diversification. By spreading your investments across different asset classes, you can potentially reduce risk and improve your long-term returns. The TSP makes diversification easy by offering a range of funds that cover various segments of the market.

To diversify your TSP portfolio:

- Consider allocating your investments across multiple funds

- Balance your portfolio between stocks (C, S, and I Funds) and bonds (F Fund)

- Include both domestic and international investments

- Adjust your allocation based on your risk tolerance and time horizon

Remember that diversification doesn’t guarantee profits or protect against losses, but it can help manage risk over time.

Understand and Utilize Lifecycle Funds

For those who prefer a hands-off approach or are unsure about managing their own investments, the TSP’s Lifecycle (L) Funds can be an excellent option. These funds automatically adjust your investment mix as you approach retirement, becoming more conservative over time.

L Funds are designed based on the year you expect to start withdrawing money. For example, if you plan to retire in 2045, you might choose the L 2045 Fund. The fund will gradually shift from a more aggressive allocation (higher stock percentage) to a more conservative one (higher bond percentage) as you near retirement.

Key benefits of L Funds include:

- Professional management of your asset allocation

- Automatic rebalancing to maintain the target allocation

- Gradual reduction of risk as you approach retirement

- Simplicity in managing your TSP investments

While L Funds offer convenience, it’s essential to ensure that the chosen fund aligns with your personal retirement goals and risk tolerance.

Maximize Your TSP Contributions

To make the most of your TSP, aim to maximize your contributions. The more you contribute, the more potential your investments have to grow over time, thanks to compound interest. Here are some strategies to boost your TSP savings:

- Contribute at least 5% of your salary to receive the full government match (for FERS employees)

- Increase your contribution percentage gradually over time

- Take advantage of catch-up contributions if you’re 50 or older

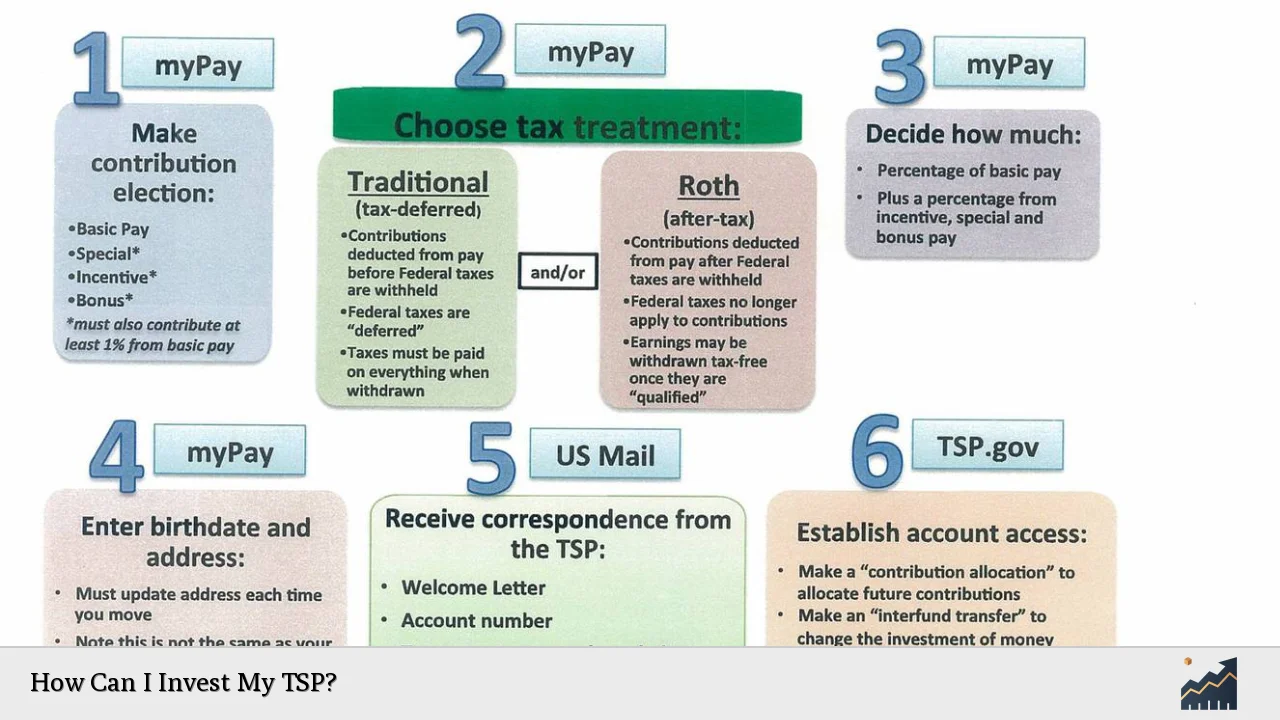

- Consider contributing to both traditional (pre-tax) and Roth (after-tax) TSP accounts

Remember, the TSP has annual contribution limits set by the IRS. For 2025, the limit is $23,500, with an additional $7,500 allowed for catch-up contributions if you’re 50 or older.

Regularly Review and Rebalance Your TSP

Investing in your TSP isn’t a one-time decision. It’s important to regularly review and rebalance your portfolio to ensure it remains aligned with your goals and risk tolerance. Market fluctuations can cause your asset allocation to drift from your target percentages over time.

To keep your TSP investments on track:

- Review your TSP account at least once a year

- Compare your current allocation to your target allocation

- Make adjustments if your allocation has drifted significantly

- Consider rebalancing if any fund’s percentage is off by 5% or more

Remember that the TSP allows you to make two free interfund transfers per month. After that, you can only move money into the G Fund for the remainder of the month.

Consider Your TSP in the Context of Your Overall Retirement Plan

While the TSP is a crucial component of your retirement savings, it’s important to consider it in the context of your overall retirement plan. This includes other retirement accounts, pensions, Social Security, and personal savings.

When planning your TSP investments:

- Assess your total retirement income needs

- Consider your other sources of retirement income

- Adjust your TSP strategy to complement your other investments

- Seek professional financial advice if needed to optimize your overall retirement plan

By taking a holistic approach to your retirement planning, you can ensure that your TSP investments work in harmony with your other financial resources to support your retirement goals.

FAQs About Investing Your TSP

- How often should I change my TSP investment allocation?

Review your allocation annually or when your financial situation changes significantly, but avoid frequent changes based on short-term market fluctuations. - Can I invest in individual stocks through my TSP?

No, the TSP only offers index funds and Lifecycle funds. For individual stock investments, consider opening a separate brokerage account. - Is it better to invest in traditional or Roth TSP?

The choice depends on your current tax situation and future expectations. Consider consulting a tax professional for personalized advice. - What should I do with my TSP if I leave federal service?

You can leave your money in the TSP, roll it over to an IRA or new employer’s plan, or withdraw it (potentially incurring taxes and penalties). - How do I protect my TSP investments during market downturns?

Maintain a diversified portfolio, consider increasing allocations to more conservative funds like the G Fund, and avoid making emotional decisions based on short-term market movements.

Investing your TSP effectively requires a combination of understanding your options, setting clear goals, and maintaining a disciplined approach. By diversifying your portfolio, maximizing your contributions, and regularly reviewing your investments, you can work towards building a strong financial foundation for your retirement. Remember that while the TSP offers powerful investment tools, it’s just one part of your overall retirement strategy. Consider seeking professional financial advice to ensure your TSP investments align with your broader financial goals and risk tolerance. With careful planning and consistent effort, you can harness the full potential of your TSP to support a secure and comfortable retirement.